Our figure of the month 05/2022: Strong increase in timber prices due to rising global demand, supply bottlenecks and trade embargoes

Forestry and sawmills benefit

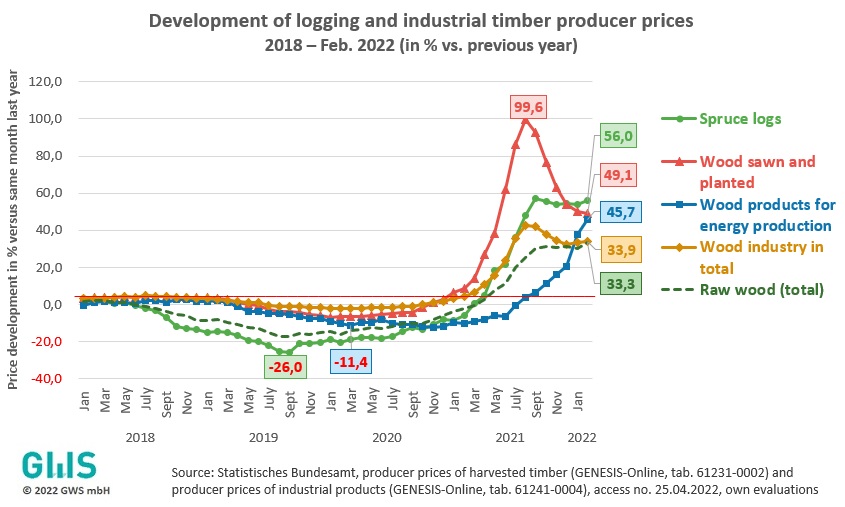

After both raw wood prices and industrial producer prices for wood in Germany stagnated for years or declined from mid-2018 to the end of 2020, they have since experienced a dynamic increase. As the figure shows, the forestry sector has benefited since the beginning of 2021 from significant price increases for raw wood overall (dark green curve) and amounted to one third most recently. For spruce wood (light green), which accounts together with fir for around three quarters of the total wood harvested from German forests, sales per cubic metre have been constantly almost 50% higher since mid-2021 compared to a year before.

Since fossil energies, above all oil and gas, have also recently become much more expensive due to Russia's war of aggression on Ukraine, among other things, wood products for energy production (blue curve) are also rising with increasing momentum at the current margin (Feb. 2022 +45.7% vs. previous year). Sawmills (Nace 16.1) have been able to realise particularly high producer price increases for sawn and planed wood (red curve), consistently almost 50% and more since mid-2021. At its peak, the producer price in this preliminary industrial stage of wood processing even doubled in August 2021.

Strong export demand and supply chain problems cause prices to rise

The timber industry benefited even more than wood owners and forestry operations from a strong increase in global demand for wood, with an overall increase in turnover of 22% in 2021 and over 40% in the export sector. After taking office in January 2021, Joe Biden launched a construction stimulus package which, together with pandemic-related supply chain problems and trade disputes, especially with Canada, led to an exponential increase in Germany's timber exports to the USA. Interrupted or delayed supply chains due to a lack of cargo ships in international maritime transport, especially to and from Asia, exacerbated the timber shortage during the pandemic and were thus a further price driver for timber.

Construction and wood-processing industries suffer

The domestic construction industry, whose demand for the renewable raw material has risen sharply in recent years, suffers particularly from this. Wooden houses are in vogue due to their advantages in terms of environmental friendliness, sustainability and - at least until 2020 - lower manufacturing costs in comparison to the classic concrete/stone construction method. Accordingly, the producer prices in the downstream, wood-processing industry are also becoming more expensive. At the current margin, more than one third more must be paid for industrial wood products overall (orange curve) compared with a year before. For other industries such as furniture manufacturers and the paper industry, which needs pulp made from wood as a raw material, the wood shortage is also leading to production bottlenecks in some cases, and the sharp rise in wood prices is putting a strain on companies' earnings.

Russia's timber trade embargo exacerbates shortage

Russia's timber export ban, which has been in effect since the beginning of 2022, further exacerbates the timber shortage on the world markets. In 2021, Russia was the largest timber exporting nation with around US$ 5.8 billion or a share of almost 50% of the total forestry and timber export value. A lifting of the embargo, especially for Western nations, is hardly to be expected in view of Putin's current war. In the short to medium term, timber prices are therefore likely to remain at a high level or rise further.

Other figures can be found here.